UK property prices dropped by 16.2% in the year following the financial crisis in 2008. This crisis stemmed a sharp growth in unemployment, as well a huge rise in the number of home-owners falling behind in mortgage payments. By the end of 2009, repossession rates had hit a 12 year high, with an estimated 46,000 people losing their homes. Now over 10 years on, we look back at the main reasons behind the huge rise in repossessions during this period, and consider that as the UK is becoming a toxic cocktail of sporadic Brexit negotiations, ever rising property prices and irresponsible lending, why it may be experiencing another property crash all over again.

Headlines from the few months following the 2008 Financial Crash

The financial crisis of 2008 originated from mortgage dealers agreeing to issue mortgages to families who could not keep up with its financially demanding terms. Much of the demographic these lenders would target would be first-time buyers that have less in-depth knowledge of the nature of loans, and therefore would not necessarily fully understand the terms of the agreement before signing the contracts. Many of these loans would have short term low interest rates. Because of these lower ‘teaser’ rates, families would take out the loan with belief they have found a good deal, and more importantly, found a way to own a home with their current salary. However, years down the line, the more demanding rates would then be triggered, resulting in the family not being able to keep up with the terms and therefore losing their home.

Ninja Loans – ‘No income, No jobs, No assets’, were commonly used prior to the financial crisis, where the lender required no income verification from the borrower, but the loan often included unfavourable terms. These types of loans are mentioned in this clip from ‘The Big Short’, depicting typical mortgage brokers shortly before the crash.

The mortgage lenders would then sell these loans to a bank, which would give the lenders money in return for the mortgages, money that lenders would then use as leverage to enable them to pay out more loans. Investment banks would buy these mortgages in bulk, which would then provide an income in the sum of all of the monthly mortgage payments. This stream of income was labelled a ‘Mortgage Backed Security’, which would be separated into hundreds, or even thousands, of smaller pieces before being sold to private investors. These smaller pieces would be wrongly presented as ‘low risk investments’. The insurance companies then found a way to get in on the act by introducing ‘Credit Default Swaps’. These Credit Default Swaps consisted of the insurance companies assuming any losses caused by mortgage-holder defaults, in return for a fee. So essentially, when people did not pay their mortgage, insurers had to pay out.

As house prices continued to rise, it appeared everyone was winning. Mortgage brokers continued to write loans everyday, banks continued to invest in ‘Mortgage Backed Security’, and home-owners continued to see their home equity rise, so they could continue to borrow on a modest salary. As the number of mortgages that were defaulted eventually increased due to the unfavourable terms, suddenly demand for houses went down, leading to them falling in price. The equity of the home owners properties had dropped, and they were unable to keep up with the hefty mortgage payments, hence they had nowhere to fall back on. Therefore, as soon as the housing bubble bursed, people lost out. Banks weren’t being paid from the mortgages they had lent out, individual investors had large sums of money in investments that were wrongly advertised as low-risk, huge banks and insurance companies were in in debt, thousands of jobs were lost, and soon enough the whole country was in crisis.

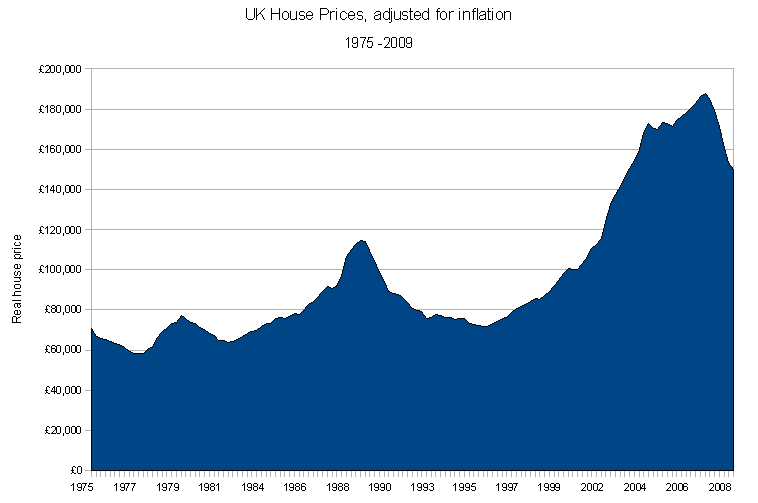

One of the main effects of the financial crisis of 2008 was the chaos it triggered in the US housing market. The crash of the housing market in the US, in time, trickled through to the UK property market, which then led to a huge rise in the number of repossessed houses in the region. Statistics from Savills, reported by uk.businessinsider.com, revealed the detrimental effects the crash had on the housing market. Housing prices dropped by 20% in 16 months, and there was a large slump in transactions levels, with the yearly amount going from an average of 1.65 million down to 730,000.

The table reflects the devastating effect the financial crisis had on UK’s housing market.

The effects seen in the UK property market are still evident today, reduced transaction levels has resulted in the total spend on house prices drop considerably. The year ending in March 2017 saw a total spend of £312 billion, £30 billion less than ten years ago.

Repossession Rates Since the Financial Crisis, a Steady Decline:

As the financial crisis was setting in, unemployment levels spiked. The scale of distress in UK mortgages began to rise, and by the end of the first half of 2018, 79,761 houses were repossessed. However, since the crisis, a number of factors have resulted in repossession rates to consistently decline. Fewer people are struggling with unemployment as the average wages are rising whilst the economy continues to recover, and the cost of mortgages are now far more stable and affordable for the average borrower, so it’s easier to get a foot on the property ladder without any deceiving agreements from the lenders.

This statement is reflected on the table below, which portrays the steady decline of mortgage repossessions from statistics reported by the Ministry of Justice.

From 1995 there was a steady decline in repossessions up until the financial crisis. This triggered a sharp rise in figures, which spiked in 2009, before starting to gradually decline again.

Brexit and Uncertainty:

Following the referendum in 2016, Britain decided to part ways with the EU, an event that has triggered a huge amount of speculation to the British economy as a whole. Many Brits are fearing the potential consequences of opting out of the EU, such as losing the workforce of immigrants, losing out on the business benefits, political controversy and a general lack of security.

Britain’s strenuous relationship with the EU has led to economic doubt and increased the chances of a property crash in the UK

Experts around the country are concluding that as departure from the EU is creeping ever closer, the UK housing market will, and in some cases already has, come to a halt.

The Financial Times reported that London’s property prices had dropped by 0.4% from May ‘17 to May ‘18, and whilst London’s prices are beginning to drop, large parts of the rest of the UK’s prices are beginning to plateau. There was a 3% rise in property prices in the same time frame, compared to 8% the year before the referendum, hinting that Brexit could possibly be playing a big part in the instability of UK’s housing market at present and, in turn, could lead to a higher number of repossessed houses.

Some of the main factors that influence the property market are wages and interest rates. These two things are likely to be effected by Brexit, however it’s not clear in what manner. If Brexit negatively affects wages, it will mean less money for mortgages, whether it’s people keeping up with payments or taking out mortgages. Less mortgages issued will mean less demand for property and therefore lower property prices as sellers will have less people to sell to. Again, this possibility may directly lead to more houses being repossessed for a number of reasons. Firstly, many that lose jobs or experience a salary reduction will simply not be able to keep up with their current mortgage demands, and secondly, because people who need to downsize due to their post-Brexit financial circumstances have far less people to sell to. Essentially, because the demand will be so low, when they try to have a quick sell of their property, they may need to let it go at a price far below market value, and possibly far below what they had needed to pay off their mortgage.

It’s not just pessimistic anticipation that is predicting Brexit to result in a repossession crisis. Neil Hudson, the director of Residential Analysts, hinted that the UK may be on the edge of a property crisis, and Brexit may be the factor to push it off. Following the slight drop in Londons property prices, Mr Hudson concluded that as things stand, borrowers can afford to wait and see if price growth recovers, as unemployment and interest rates remain low. However, if there is an economic shock of some sort which leads to a rise in unemployment in London, it could swiftly result in a property price plunge. Considering this, as negotiations continue to be pragmatic, Brexit may be that economic shock that catalysis this plunge. Mike Carney, the governor of the bank of England, helped confirmed these suspicions as he has warned senior ministers that Brexit could lead to a property crisis in the UK. Mr Carney even compared the current situation to the 2008 financial crash, as Britain’s relationship with the EU continues to be strained.

“If there was a big economic shock, then all bets are off’”

Mr Hudson, director at Residential Analysts, on possible factors that could contribute to a heavy decline in UK’s property prices

The Ticking Time Bomb of a Mortgage Crisis:

Although the days of questionable mortgage loans being issued appear to be over following the stricter regulations subsequent to the financial crisis, as well as abolishment of stamp-duty for first time buyers, it’s evident that many borrowers are still in danger of losing their homes, without being completely aware of it. An article from the BBC revealed that the FCA have released a warning that many borrowers are ignoring a mortgage time bomb, and hundreds of thousands could be at risk of having their homes repossessed.

“We are very concerned that a significant number of interest-only customers may not be able to repay the capital at the end of the mortgage and be at risk of losing their homes”

Jonathan Davidson – executive director of supervision at the FCA credit.

The reason behind this warning from the FCA, that would be a surprise to some considering the strict regulations to qualify for a mortgage at present, is down to ‘interest only home loans’. According to the FCA, one in five mortgages come under the ‘interest only loan homes’, which terms allow borrowers to pay off the amount borrowed when the mortgage term ends as a final lump sum. They stated that many of these types of loans will be coming to an end in the next 10 to 14 years, and observations have found that many of the borrowers have been ignoring letters from the lenders. Further research was conducted to learn why so many borrowers were ignoring letters – which revealed that many believed they had an adequate payment plan in place, whilst others did not trust the lenders and therefore were suspicious of the letter, and some simply ignored the warning leaving it for tomorrows problem.

This has not been the only warning the FCA has recently released, as it’s mentioned those that took out mortgages years ago, before cheaper mortgage rates were introduced, are ‘mortgage prisoners’ and ‘trapped’ to their contracts with demanding terms. So if you assume that current home owners that still have high exposure on their mortgage probably won’t be in any trouble, as It’s been over 10 years since the financial crisis and rules are far stricter now with lenders issuing mortgages, you may be inaccurate with your assumption. Lenders were handing out dubious mortgages excessively prior to the financial crisis, many of those mortgages are now entering biting point and therefore some individuals may be facing repossession in the near future.

As mentioned previously in the article, there are far fewer transactions now in the property market than there were in the past. There could be a number of reasons behind this away from the referendum – the removal of stamp-duty for some first time buyers could mean that many that move into their first property may be more inclined to stay residing their, due to the expense of stamp duty if they were to move on, so they could decide an extensive refurbishment could suffice over buying a new property all together. In addition, mortgages are simply harder to land now, so there could be less demand in general. Alternatively, it could be the uncertainty as a whole that is making people less willing to sell now, as they are waiting to see how the next year or so pans out for property prices. Whichever way you look at it, and whatever factor you allocate blame to, the simple fact is that less transactions indicate low activity and therefore a weakness in the UK’s property market.

Fewer people appear to be buying property due to uncertainty with the UK’s future house prices and Brexit.

Ten years ago people on modest incomes were able to secure mortgages, and therefore did not need to turn to alternative routes to fund their first property. However, due to the new regulations of qualifying for a mortgage, people in a lower wage bracket can no longer rely on this to help them onto the property ladder. This has certainly increased the reliance on the bank of mum and dad for many individuals, however it’s also increased the popularity of unsecured credit. Unsecured credit provides an alternative opportunity to borrow, however it is both higher in risk and more expensive.

Thisismoney.co.uk analysed figures from the Bank of England that revealed the rate of spend on credit card in 2017 was the highest it had been for over 10 years. This suggests that the decline in mortgage lending has triggered a rise in unsecured credit, and another way of wording that is, low cost borrowing is declining and high cost borrowing is increasing. As this is the case, there will be slightly less disposable income for borrowers to spend on other companies products, eating out in restaurants and buying stock from high-street stores, which all helps stabilise the economy. If the money going into the economy reduces for this reason, it will have a negative effect on the economy a a whole, lead to lower salaries and higher unemployment levels and therefore could lead to more distressed properties.

Mortgage approvals being reduced has led to a steady increase in credit card lending over the last few year, a more expensive means of borrowing

It may be a slightly pessimistic outlook, but is appears that in 2008 the economy crashed so badly that it was considered by many as the worst financial crisis since the great depression in the 1930’s. We are now ten years on and, judging from the current scenario, we have learned absolutely nothing. Bad mortgage debt has been shifted to other types of lending following changes in mortgage regulations, large banks still control the vast majority of capital and trading in the financial market is still as prominent as ever. Maybe there is a ticking time bomb and we will be in a financial crisis within the next 5 years, and that will trigger a large number of repossessions, or maybe there won’t be a financial crisis but due to demanding mortgages or a slight dip in the UK’s property prices, there will be a repossession crisis nonetheless.

As for the property market and repossessions, if you want to get on the property ladder or build a property portfolio, then try to do so. There’s negative press at the moment regarding the property market but this can be inaccurate and just because there are fewer transactions it does not necessarily indicate it’s a bad time to invest in property. Rent demand is as high as ever, and as the younger generation have a growing opportunity of working abroad, back-packing on the cheap and a reduced desire to stay in one place for a number of years at a time, I can’t see this demand reducing any time soon. Alternatively, if you simply are looking to buy for a new home, it’s helpful to stay informed of property prices and developments in the property market. Don’t be afraid to re-locate if it means you are buying in an area where prices are thriving, utilise every available gate-way that sources property, whether it be Estate Agents or online tools, and remember to conduct extensive due-diligence on any form of borrowing you may need to help fund the purchase.

Essentially, whichever way you look at it, and regardless of how well you may know the industry, it’s impossible to call. The most sensible and pro-active thing to do at present is to remain positive, yet cautious. No one wants to spend their life anticipating a crisis over the hill and therefore be penny counting and withdraw from certain markets. It’s important to go out, spend money in different companies, restaurants, shops, bars, this in itself assists the economy and minimises the chances of both a financial and repossession crisis in years to come.